Working capital is one of the most important indicators of a company’s financial health. It reflects whether the business can meet its short-term obligations and support ongoing operations.

While the formula is simple – current assets minus current liabilities – the real insight lies in how working capital connects to cash flow, performance metrics, and the Cash Conversion Cycle (CCC).

Strong working capital management ensures a company can convert inventory and receivables into cash while paying suppliers efficiently. The CCC highlights how quickly this conversion happens, showing whether capital is tied up too long in operations or working efficiently to support growth.

In this article, we’ll explain what working capital is, break down its components, and explore how it influences cash flow, liquidity, and profitability.

We’ll also cover why monitoring key working capital metrics and the CCC is essential, and why looking beyond accounting definitions to Operating Working Capital provides a more practical view of business efficiency.

Want to go beyond the basics?

Become a Certified Working Capital Expert with our CPD accredited course Managing Working Capital

Working Capital, also referred to as Net Working Capital (NWC), represents the capital a company has available to meet its short-term financial obligations.

From a cash flow perspective, current assets and current liabilities behave very differently.

| Item | Description |

|---|---|

| Current Assets | Typically represent areas where a company has tied up or invested cash as part of its operations - for example through inventory purchases, customer credit, or prepaid expenses. |

| Current Liabilities | Represent obligations where payment has not yet been made. These liabilities therefore act as short-term sources of operational funding by postponing cash outflows. |

Working capital therefore reflects the balance between:

This is one of the reasons why working capital plays such an important role in liquidity, cash flow, and operational performance.

The working capital metric helps assess whether a company holds sufficient short-term assets to meet its short-term financial obligations and support day-to-day operations.

These short-term assets may include cash itself, as well as cash equivalents such as inventory and accounts receivable that are expected to convert into cash within one operating cycle.

Working capital is therefore calculated by subtracting current liabilities from current assets.

Working Capital Formula:

Working Capital = Current Assets – Current Liabilities

| Item | Amount (Example 1): | Amount (Example 2): |

|---|---|---|

| Current Assets | $12 million | $9 million |

| Current Liabilities | $8 million | $10 million |

| Working Capital | $4 million ($12m - $8m) | -$1 million ($9m - $10m) |

In our first example, the company has $4 million in positive working capital, meaning its short-term assets exceed its short-term obligations.

This generally indicates sufficient liquidity to support day-to-day operations and meet near-term financial commitments.

However, positive working capital alone does not automatically indicate strong performance. Excess inventory, slow-moving receivables, or unnecessary cash buffers may still suggest inefficient capital utilization or operational inefficiencies.

Importantly, not all current assets are equally liquid or readily convertible into cash. As a result, a company may appear financially healthy from a working capital perspective while still experiencing operational inefficiencies or underlying liquidity constraints.

In the second example, the company has negative working capital of $1 million, meaning its short-term liabilities exceed its short-term assets.

This can indicate liquidity pressure and a reduced ability to meet short-term financial obligations using existing current assets alone.

However, negative working capital is not always a sign of poor performance. In some business models – such as grocery retail, e-commerce, or subscription-based businesses – companies may operate successfully with negative working capital due to fast inventory turnover, strong cash generation, or favorable customer and supplier payment terms.

The underlying drivers and operational context therefore matter significantly when interpreting working capital performance.

As these examples illustrate, working capital should always be interpreted in the context of a company’s business model, operating structure, and cash flow dynamics – not simply as a standalone balance sheet number.

It is therefore important to understand the individual components that make up current assets and current liabilities, as these are influenced by very different operational, commercial, financial, and accounting drivers.

All working capital components can be found on a company’s balance sheet, under current assets and current liabilities.

Current assets refer to shorter-term assets that a company owns, benefits from, or uses to generate income from.

These assets are considered current as they are expected to be consumed or converted into cash within an operating cycle – most often within a year.

These assets are used to facilitate day-to-day operational activities and expenses, and include the company’s cash, inventories, accounts receivable, pre-paid expenses and other current assets.

The table below outlines the most common current asset categories and their primary drivers.

| Item | Description | Primary Driver |

|---|---|---|

| Cash | Includes all the money a company has on hand. | Financial |

| Inventory | The value of raw materials, work in progress, and finished goods held by the company. | Operational |

| Accounts Receivable | Outstanding customer invoices that have not yet been paid. | Operational / Commercial |

| Accrued Revenue | Income that a company has earned by delivering goods or services but has not yet invoiced or received payment for. | Operational / Accounting |

| Pre-paid Expenses | Includes the combined value of all expenses that have been paid for in advance, but have not yet incurred (e.g., supplier pre-payments). | Operational / Financial |

| Other Current Assets | This balance includes the combined value of current assets that are considered uncommon or otherwise insignificant to the business. | Mixed |

While all current assets impact liquidity, the underlying drivers differ significantly.

Some components are primarily operational and influenced by planning, demand, and execution, while others are more financial or accounting-oriented in nature.

This distinction becomes especially important when analyzing operating working capital.

Current liabilities refer to short-term obligations that a company is expected to settle within one operating cycle – typically within 12 months.

These liabilities arise through day-to-day operations, financing activities, and commercial transactions, and play an important role in short-term liquidity and cash flow management.

Current liabilities include items such as accounts payable, unearned revenue, wages payable, the current portion of long-term debt, unpaid taxes, and other short-term debt due within one year.

The table below summarizes the most common current liabilities found on the balance sheet.

| Item | Description | Primary Driver |

|---|---|---|

| Accounts Payable | Outstanding supplier invoices for goods and services received but not yet paid. | Operational / Procurement |

| Accrued Expenses | Expenses incurred but not yet invoiced or paid, such as salaries, utilities, freight, or operational services. | Operational / Financial |

| Unearned Revenue | Payments received from customers before goods or services have been delivered. | Operational / Commercial |

| Short-term Debt | Loans, credit facilities, or borrowings due within 12 months. | Financial |

| Current Portion of Long-term Debt | The share of long-term borrowings that becomes due within the next 12 months. | Financial |

| Taxes Payable | Taxes owed to authorities but not yet paid, such as VAT, payroll tax, or income tax liabilities. | Financial |

| Other Current Liabilities | This balance includes the combined value of current liabilities that are considered uncommon or otherwise insignificant to the business. | Mixed |

While all current liabilities impact short-term liquidity, the underlying drivers vary significantly.

Some liabilities are closely linked to day-to-day operations and commercial activity, while others are primarily financial or regulatory in nature.

Understanding these distinctions is important when analyzing operating working capital and identifying the drivers of cash performance.

Many companies analyze working capital purely from a financial or accounting perspective. In practice, however, the largest working capital drivers are often operational – shaped by forecasting accuracy, lead times, inventory policies, customer behavior, and payment terms.

Understanding which components are operational, commercial, financial, or accounting-driven is essential when managing operating working capital effectively.

Read more on working capital drivers here.

Working capital is often associated with short-term liquidity and the ability to pay near-term obligations. In practice, however, working capital plays a much broader role in business performance.

Well-managed working capital supports not only liquidity, but also operational efficiency, strategic flexibility, resilience, and profitability. Its importance extends across strategic, tactical, and operational decision-making throughout the business.

The table below outlines how working capital influences each of these perspectives.

| Perspective | Focus | Why it matters |

|---|---|---|

| Strategic | Ensuring operating working capital supports the company’s long-term direction, resilience, and return objectives. | Strong working capital performance supports growth, profitability, resilience, and efficient capital allocation. |

| Tactical | Ensuring sufficient liquidity and cash flow to meet short-term operational costs and financial obligations. | Effective working capital management reduces liquidity risk and improves short-term financial stability. |

| Operational | Ensuring working capital supports efficient day-to-day execution while minimizing friction, delays, excess buffers, and operational waste. | Well-managed working capital improves operational flow, agility, responsiveness, and the ability to adapt to changing demand and supply conditions. |

Importantly, the different dimensions of working capital are not driven by the same underlying components.

Poor working capital management can create unnecessary operational friction, weaken liquidity, increase financing dependency, and limit a company’s ability to respond effectively to changing market conditions.

Conversely, companies with strong working capital practices are often better positioned to support growth, absorb disruption, and operate with greater flexibility and resilience. They typically operate with less friction, waste, and unnecessary capital lock-up – allowing resources to be directed toward the areas that generate the highest strategic and financial return.

Strong working capital management is ultimately about balancing liquidity, profitability, growth, resilience, and operational performance in a sustainable way.

Importantly, companies seeking to improve the strategic and operational dimensions of working capital must look beyond the traditional working capital metric and focus on operating working capital instead.

You can read more about this under Limitations of the Working Capital Metric below.

A company’s ability to generate cash flow is heavily influenced by how efficiently it manages its working capital.

Without sufficient available cash, a company may struggle to perform routine activities such as purchasing goods and services, paying employee salaries, making investments, financing growth, or servicing debt.

Imagine a company that improves operating profit by $20 million during the year.

At first glance, we might expect operating cash flow to increase by the same amount.

However, suppose the company also needed to:

This means an additional $25 million of cash is now tied up in working capital.

As a result, the additional working capital requirement would more than offset the increase in operating profit, resulting in a net operating cash flow impact of -$5 million.

| Item | Cash flow impact |

|---|---|

| Increase in Operating Profit | +$20m |

| Increase in Inventory | -$10 million |

| Increase in Accounts Receivable | -$15 million |

| Net Operating Cash Flow Impact | -$5 million |

Although the company generated higher profit, the business actually consumed cash during the period because more capital became tied up in operations.

Want to explore the relationship between working capital and cash flow in more detail?

Read: Working Capital & Cash Flow | Definition, Relationship and Business Application

There is no universal definition of a “good” working capital level.

Working capital requirements vary significantly across industries and can even differ between companies operating within the same sector.

Several factors influence these differences, including:

| Structural Driver | How It Influences Working Capital Requirements |

|---|---|

| Commercial Terms & Market Practices | Industry standards, regional norms, and customer expectations influence payment terms, receivables levels, and cash collection timing. |

| Supply Chain & Sourcing Structure | Global sourcing, supplier locations, and replenishment models influence inventory requirements, lead times, and cash tied up in transit. |

| Production & Operational Model | Long production cycles, operational complexity, and multi-stage processes often require larger inventory buffers and working capital support. |

| Service Level & Resilience Requirements | Companies prioritizing high service levels, responsiveness, or supply chain resilience may intentionally hold additional inventory and operational buffers. |

| Business Model & Cash Flow Characteristics | Different business models generate, collect, and retain cash differently, creating structurally different working capital dynamics. |

| Growth Strategy & Expansion Plans | Rapid growth, market expansion, or scaling activities often increase working capital requirements as operations and sales volumes expand. |

Importantly, many of these factors reflect operational and commercial realities rather than inefficiencies alone and are therefore often structurally embedded in the company’s operating model.

Customer locations, supplier structures, replenishment lead times, service expectations, and business model requirements all influence the amount of working capital a company naturally requires to operate effectively.

For example:

These structural conditions and operational constraints help shape the company’s working capital requirements and liquidity needs.

Operating significantly above or below these levels may create inefficiencies:

As a result, effective working capital management is not simply about minimizing working capital, but about finding a level that appropriately balances liquidity, operational performance, resilience, growth, and profitability. This is what we call the working capital Setpoint.

Want to explore this concept further?

Read: The Operating Working Capital Setpoint | Finding the Sweet Spot Between Cash, Growth, and Resilience

Learn how structural constraints, operational realities, and strategic trade-offs shape the optimal level of operating working capital.

Despite these differences, all companies must maintain sufficient liquidity to meet short-term financial obligations and support day-to-day operations.

Poorly managed working capital can create operational pressure, increase financing dependency, and reduce a company’s financial flexibility and resilience.

To better understand and monitor working capital performance, companies often use a range of financial and operational metrics. These metrics help evaluate liquidity, capital efficiency, operational efficiency, and the amount of cash tied up in day-to-day operations.

Importantly, different metrics serve different purposes depending on whether the focus is strategic, tactical, or operational.

| Perspective | Focus | Typical KPI Examples |

|---|---|---|

| Strategic | Evaluating capital efficiency, profitability, and long-term value creation | Working Capital as % of Revenue, Return on Working Capital |

| Tactical | Monitoring liquidity and short-term funding capacity | Working Capital Ratio (Current Ratio) |

| Operational | Monitoring day-to-day cash flow efficiency and operational flow | Cash Conversion Cycle (CCC), DIO, DSO, DPO |

As a result, no single metric provides a complete view of working capital performance. Different KPIs should instead be interpreted together and in the context of the company’s business model, operational structure, cash flow characteristics, and strategic priorities.

Many companies also analyze working capital relative to revenue to better understand how much capital is tied up in operations compared to the size of the business.

The metric is commonly calculated as:

Working Capital % of Revenue Formula:

Working Capital % of Revenue = Working Capital / Revenue

This metric helps illustrate how operationally cash-intensive a business is and how efficiently working capital supports revenue generation.

In general:

However, the optimal level depends heavily on industry structure, inventory requirements, customer payment terms, supplier arrangements, operational complexity, and overall business strategy.

For this reason, companies should focus not only on reducing working capital, but on finding a working capital level that appropriately balances liquidity, operational performance, growth, resilience, and profitability.

Many companies track their Working Capital Ratio – also referred to as the Current Ratio – to monitor short-term liquidity and the company’s ability to meet near-term financial obligations.

The ratio is calculated as:

Working Capital Ratio Formula:

Current Ratio = Current Assets / Current Liabilities

The metric measures how much short-term asset coverage a company has relative to its short-term liabilities.

In practice, the current ratio helps indicate whether a company is likely to hold sufficient short-term assets to support upcoming payment obligations and day-to-day operational funding needs.

For example:

However, the optimal ratio varies significantly depending on industry, business model, operational structure, and cash flow characteristics.

Importantly, a high current ratio does not automatically indicate strong working capital performance. Excess inventory, slow-moving receivables, or unnecessary cash buffers may still indicate inefficient capital utilization or operational inefficiencies.

Similarly, some companies may successfully operate with lower current ratios due to fast inventory turnover, strong cash generation, or favorable customer and supplier payment structures.

As a result, working capital metrics should always be interpreted in the context of the company’s operating model and cash flow dynamics.

From an operational perspective, many companies also monitor the Cash Conversion Cycle (CCC), which measures how efficiently cash moves through inventory, receivables, and payables.

The Cash Conversion Cycle is commonly analyzed through:

Together, these metrics help companies understand how operational decisions influence cash flow, liquidity, responsiveness, and working capital efficiency.

Unlike more static balance sheet metrics, operational working capital metrics help illustrate how efficiently cash moves through day-to-day operations and how quickly invested capital is converted back into available cash.

Want to explore the Cash Conversion Cycle further?

Read: Cash Conversion Cycle (CCC) | Definition, Formula and Business Application

Here you can learn more about Days Inventory Outstanding, Days Sales Outstanding and Days Payables Outstanding – to better understand how inventory, receivables, and payables individually influence working capital performance and operating cash flow.

Although working capital is widely used to assess liquidity and short-term financial health, the metric has important limitations when evaluating operational performance.

This is because traditional working capital includes a mix of:

As a result, the metric alone may not clearly reflect how efficiently a company manages its core operating activities.

For example, balances such as excess cash, short-term debt, tax liabilities, or other non-operational items can significantly influence the working capital position without necessarily reflecting operational efficiency or cash flow performance.

In addition, not all current assets are equally liquid or easily converted into cash. Excess inventory, slow-moving receivables, or accounting-related accruals may create a misleading picture of liquidity and operational performance when viewed only through the traditional working capital metric.

To better evaluate the operational drivers of working capital, many companies instead focus on Operating Working Capital (OWC) – also referred to as Trade Working Capital.

Operating working capital isolates the balances directly linked to day-to-day business operations, such as:

As a result, OWC provides a clearer view of how operational decisions, commercial structures, and supply chain performance influence liquidity, cash flow, and capital efficiency.

Because of this, operating working capital is often considered a more actionable and operationally relevant metric for managing working capital performance.

Want to learn more?

Read: What Is Operating Working Capital? | Definition, Formula and Business Application

Learn how operating working capital differs from traditional working capital – and why many companies use OWC to evaluate operational efficiency, liquidity, and cash flow performance.

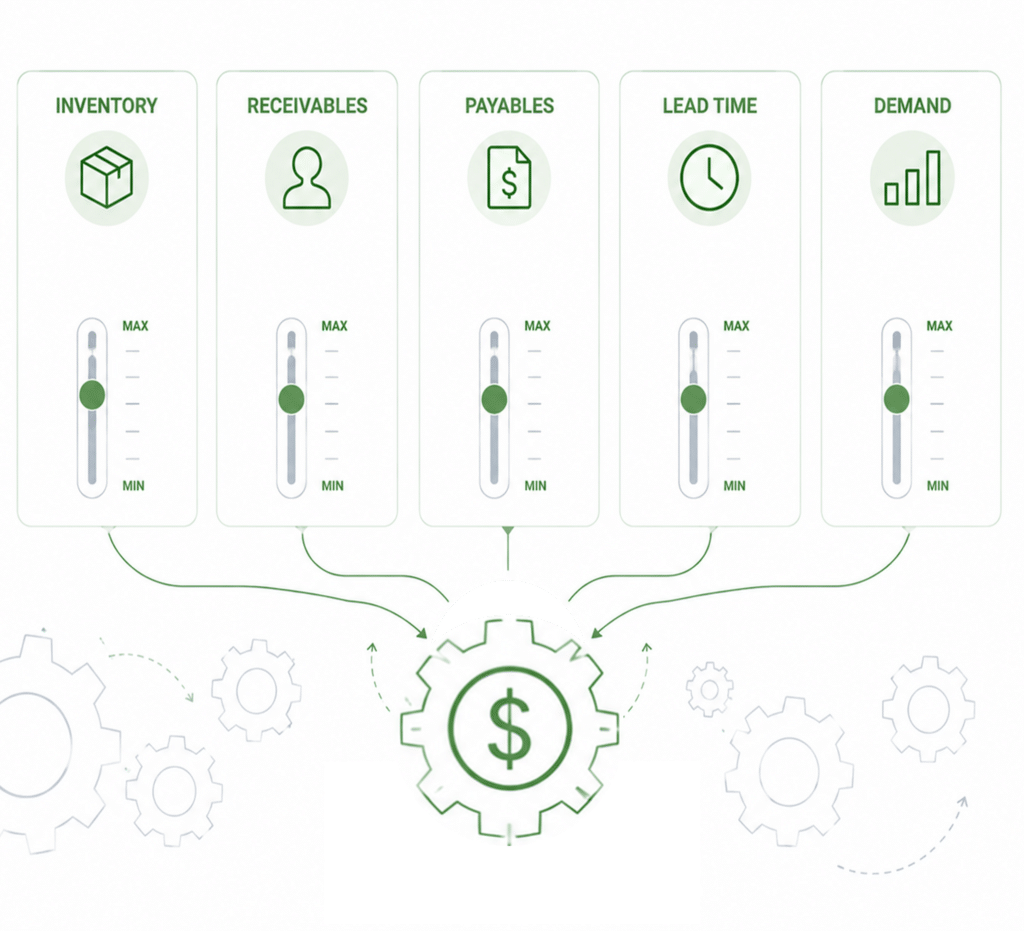

Improving the working capital involves managing your current assets and liabilities more effectively to ensure you have enough liquidity to cover short-term obligations. Here are some strategies to improve your working capital:

Want to learn more about inventory management? Check out Working Capital Hub’s complete guide here.

Want to learn more about receivables management? Check out Working Capital Hub’s complete guide here.

Want to learn more about payables management? Check out Working Capital Hub’s complete guide here.

By implementing the above strategies, a company will improve its working capital and strengthen its financial position, ultimately enhancing its ability to meet short-term obligations and support long-term growth.

Working capital is far more than a line item on the balance sheet – it is a vital indicator of a company’s liquidity, efficiency, and financial health.

By understanding its components, monitoring key ratios, and recognizing its impact on cash flow and the cash conversion cycle, businesses can identify risks early and unlock opportunities for growth.

Strong working capital management means finding the right balance: enough liquidity to cover obligations, but not so much idle capital that resources go underutilized.

Ultimately, mastering working capital equips companies with the agility to sustain operations, fund growth, and strengthen long-term profitability.

Turn theory into practice and boost your career with accredited training. Become a Certified Working Capital Expert by enrolling in our flagship course: Managing Working Capital.

Categories