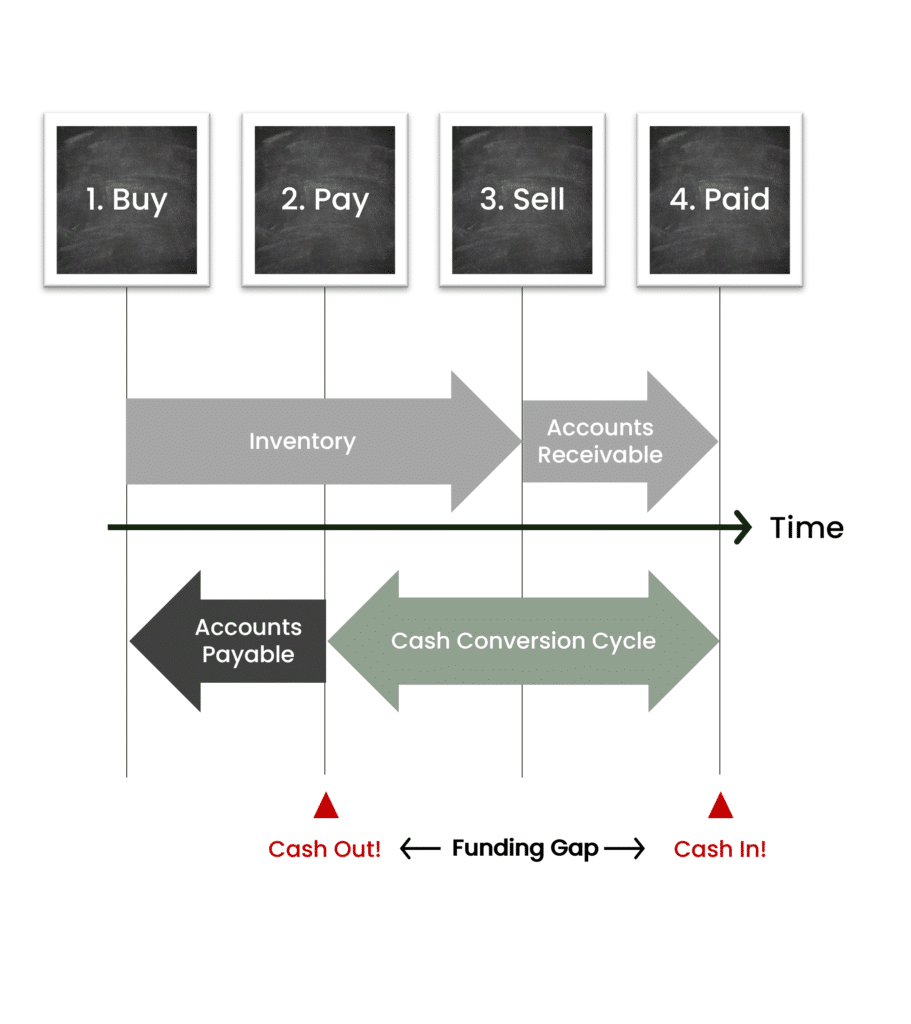

Even though the Cash Conversion Cycle is measured in days, its real impact can be translated into cash.

This is what makes the metric so useful in practice: it helps illustrate why even a seemingly small improvement can be meaningful.

Every one-day reduction in CCC releases the cash equivalent of one day of operating activity.

As a rough rule of thumb:

Cash value of 1 CCC day ≈ Annual revenue ÷ 365

In our simplified example above, that means:

100,000 ÷ 365 ≈ 274

So a one-day improvement in the Cash Conversion Cycle would release approximately $274,000 of cash.

A 10-day improvement would therefore release approximately $2,740,000.

This helps put the metric into practical terms.

Even a modest reduction in inventory days, receivables days, or an improvement in supplier payment terms can release real liquidity from the business.

That cash can then be used for:

- growth investments

- debt reduction

- resilience and liquidity buffer

- reducing reliance on external financing

However, not every day in the Cash Conversion Cycle should automatically be removed.

Some working capital is structurally required to support a company’s operating model, service levels and commercial position.

The most valuable CCC improvements are therefore not the fastest ones, but the ones that are sustainable, structurally sound, and aligned with the business’s working capital setpoint.