Cash is the oxygen of business. A company can report strong profits but still face financial distress if it cannot generate enough cash to cover its day-to-day obligations. Salaries, supplier payments, loan repayments, and investments all require cash, not just accounting profit.

One of the most critical links between profit and cash is Working Capital. More precisely, Operating Working Capital (OWC) shows how much money a company has tied up in receivables, payables, and inventory.

The speed at which these items are turned into cash is measured by the Cash Conversion Cycle (CCC) – the time it takes to convert outflows for inventory and payables into inflows from customer payments.

A longer CCC means cash is tied up for extended periods, negatively impacting a company’s cashflow. A shorter CCC means a company can recycle its cash faster, providing more flexibility for reinvestment and resilience.

Managing both the level of OWC and the efficiency of the CCC can make the difference between a company that is constantly short of liquidity and one that enjoys the flexibility to invest, grow, and weather shocks.

This fact sheet explains the relationship between operating working capital and cashflow, outlines the drivers that affect both, and illustrates the impact through clear examples.

Key Take Aways

Profits do not equal cash flow. Companies can report accounting profits but still run out of cash if working capital is inefficiently managed.

Working Capital = Current Assets – Current Liabilities.

Without generating enough cashflow, a company will find it difficult to conduct routine activities such as buying goods and services, paying its employee salaries, making investments, financing growth, or paying off debt.

Cash is in turn directly affected by a company’s ability to convert its net operating working capital assets into sales and customer payments.

Cashflow problems are a leading cause of corporate distress. Multiple studies highlight that many bankruptcies occur not because companies are unprofitable, but because they run out of cash.

Consider two businesses:

Both report healthy profits on their income statement.

Yet one struggles to pay suppliers because too much cash is tied up in inventory and overdue receivables.

The other, with efficient operating working capital management, enjoys liquidity that allows it to reinvest in growth.

The lesson: profitability does not guarantee liquidity. The bridge between profit and cash is operating working capital.

What is Working Capital?

Working Capital measures short-term financial health by comparing assets that can be quickly converted into cash with liabilities that must be paid soon:

Working Capital = Current Assets – Current Liabilities

While this broad measure includes items like cash and debt, financial managers often focus on Operating Working Capital (OWC) to evaluate liquidity from operations:

This definition focuses on how a company finances its operations:

Inventory = goods waiting to be sold.

Accounts Receivable (AR) = what customers owe.

Accounts Payable (AP) = what the company owes suppliers.

Together, these determine how much cash is tied up in running the business.

What is Cashflow?

Cash flow represents the net movement of money into and out of a business over a given period. It is not the same as profit.

A company may show profits on its income statement while still running out of cash if payments from customers are delayed, if inventory levels are high, or if large investments have been made.

Cash flow is detailed in the Cashflow Statement, which is divided into three main sections:

1. Cashflow from Operating Activities

Cash generated from the company’s core day-to-day operations.

Includes revenues collected from customers, payments to suppliers, wages, taxes, and changes in Operating Working Capital (OWC).

This is the most direct measure of whether a company’s operations generate sufficient cash to sustain itself.

2. Cashflow from Investing Activities

Cash used to acquire, or received from selling, long-term assets such as property, plants, equipment, or financial investments.

A negative Investing Cashflow is not necessarily bad – it often indicates growth through reinvestment.

3. Cashflow from Financing Activities

Cash flows between the business and its owners or lenders.

This includes raising capital (issuing shares, borrowing funds) and outflows such as dividends or debt repayments.

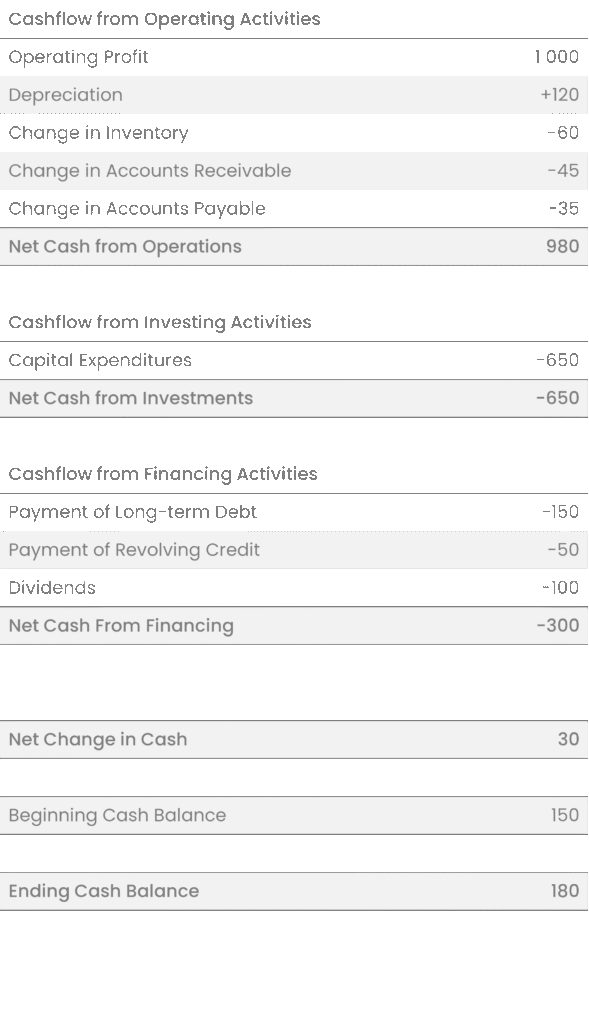

Example: Cashflow Statement

Of these, Operating Cash Flow is the most critical for day-to-day survival. It shows how much cash a company’s normal business activities generate after considering working capital needs.

Example: Profit vs Cashflow

A company sells $1 million worth of products in a quarter, but only half is paid in cash while the rest is on credit.

On the income statement, profit may look strong, but the cashflow statement shows only $500,000 in actual inflows.

If at the same time inventory increases and suppliers are paid early, the company may even report negative operating cash flow despite being profitable.

The Relationship Between Working Capital and Cashflow

The link between Working Capital and Cashflow is straightforward but powerful: how a company manages receivables, payables, and inventory directly determines how much cash it has available

When Operating Working Capital (OWC) increases:

More money is tied up in accounts receivable (customers paying slower).

More cash is locked into inventory (stock not yet sold).

Less cash is available from accounts payable (suppliers are paid faster).

This formula highlights that profits alone do not equal cash. Depreciation and amortization are added back (they are non-cash expenses), while changes in OWC adjust for the timing of cash inflows and outflows from operations.

Why It Matters

Two companies with the same sales and profit can have dramatically different liquidity positions depending on how they manage OWC.

For example:

A company with slow-paying customers and high inventory may struggle to pay bills despite being profitable.

Another company with efficient collections and lean inventory may enjoy strong cash flow even with identical profit margins.

Key Insight

Operating Working Capital is the bridge between profit and cash flow. Efficient management of OWC ensures that accounting profits are actually converted into usable cash, which is critical for liquidity, resilience, and growth.

What Drives Changes in OWC?

Movements in OWC are driven by three direct levers – Accounts Receivable, Inventory, and Accounts Payable – plus a set of structural and external drivers that influence those levers.

The direct levers explain what changes immediately in operating working capital.

The structural and external drivers explain why those changes occur.

Direct Levers

Inventory:

Increase in Inventory (cash outflow): Seasonal buildup, higher safety stock, poor forecasting, or slow-moving goods.

Decrease in Inventory (cash inflow): Lean production, better demand planning, and faster turnover free up cash.

Accounts Receivable (AR):

Increase in AR (cash outflow): Customers take longer to pay, customers receive longer payment terms, or more sales are made on credit.

Decrease in AR (cash inflow): Customers pay faster, or stricter credit terms are enforced.

Accounts Payable (AP):

Increase in AP (cash inflow): Extending or renegotiating supplier terms conserves cash.

Decrease in AP (cash outflow): Paying suppliers earlier reduces liquidity.

Structural and External Drivers - Why OWC Changes

While AR, Inventory, and AP are the immediate levers, several underlying forces determine how they behave:

Market and Customer Mix

Different industries, regions, and customer segments have varying credit norms.

Example: Entering a market with innately longer customer credit terms will cause an increase in Accounts Receivable.

Why it matters: Strategic choices about markets and customers directly shape the company’s cash cycle.

Supplier and Operational Efficiency

Inefficiencies inside or outside the company raise operating working capital needs.

Example: Poor supplier reliability forces a company to hold extra safety stock; poor internal quality leads to more disputed invoices, delaying collections.

Why it matters: Operational weaknesses convert into higher OWC, meaning cash gets tied up instead of being free for growth.

Seasonality

Many businesses experience predictable swings in demand.

Example: Retailers build inventory before the holiday season; agricultural businesses see spikes around harvests.

Why it matters: Companies must plan cash reserves and financing around seasonal peaks in OWC, or risk liquidity crunches during buildup periods.

Growth and Expansion

Rapid growth almost always requires additional operating working capital.

Example: a company growing 20% in sales will see its operating working capital grow 20% (or more), assuming no changes to its inherent supply chain conditions and constraints.

Why it matters: Growth can consume cash faster than profit generates it. Without planning, high growth may create cash shortages.

Key Insight

Structural and external drivers explain why working capital shifts over time. They highlight that managing OWC is not only about internal process control but also about adapting to market realities, operational efficiency, seasonality, and growth pressures.

Companies that anticipate these drivers can adjust early (e.g., negotiate better terms, align financing to seasonal cycles, or improve supply chain reliability) and avoid being surprised by sudden cash constraints.

Case Example: Two Companies, Same Profit – Different Cash Outcomes

Two manufacturing companies report identical sales and operating profit. At first glance, they look equally healthy.

However, differences in how they manage Operating Working Capital (OWC) dramatically change their cash position.

What Happened?

Company A increased its OWC by $5m. Perhaps customers paid later, or inventory levels grew. This tied up more cash in operations, reducing available cash flow to $15m.

Company B reduced its OWC by $5m. It may have collected receivables faster, optimized stock, or negotiated better supplier terms. This freed up cash, boosting operating cash flow to $25m.

Why It Matters

Both firms show the same profit, but Company B has $10m more cash available at year-end. This difference is not just an accounting technicality – it can decide whether a company can:

Repay debt on time.

Invest in growth opportunities.

Withstand unexpected shocks.

Key Lesson

Profits do not equal cash.

How effectively a company manages receivables, payables, and inventory (it’s OWC) is often the difference between thriving and struggling.

Tips on Managing Operating Working Capital to Improve Cashflow

Improving cash flow requires more than just focusing on receivables or delaying supplier payments.

It’s about holistic management of the Cash Conversion Cycle (CCC) – the time it takes to turn investments in inventory and receivables into cash, minus the time taken to pay suppliers.

By tackling each element of working capital in a structured way, companies can free up liquidity without harming operations.

1. Accelerate Receivables (DSO – Days Sales Outstanding)

Tighten credit checks before extending terms to customers.

Incentivize early payments through discounts or digital payment solutions.

Enforce payment terms consistently to avoid creeping delays.

Use analytics to identify slow-paying customers early.

Impact on CCC: Shorter DSO reduces the cash tied up in receivables, improving liquidity.

2. Optimize Inventory (DIO – Days Inventory Outstanding)

Improve forecasting accuracy by integrating demand planning with real-time sales data.

Leverage S&OP (Sales & Operations Planning) to align demand, production, and supply decisions across functions.

Reduce obsolete or slow-moving stock with regular portfolio reviews.

Collaborate with suppliers to shorten lead times and enable just-in-time deliveries.

Impact on CCC: Lower DIO means less money trapped in stock, freeing cash without risking stockouts.

3. Negotiate Payables (DPO – Days Payables Outstanding)

Extend terms responsibly where possible, aligning with industry benchmarks.

Collaborate with strategic suppliers to balance cash needs with long-term partnerships.

Consider Supply Chain Finance (SCF) solutions to extend DPO while giving suppliers early payment options.

Impact on CCC: Higher DPO allows the company to hold onto cash longer, but must be balanced against supplier relationships and reputation.

4. Streamline Processes

Order-to-Cash (O2C): Reduce errors, automate invoicing, and integrate with customer systems to accelerate payments.

Procure-to-Pay (P2P): Digitize procurement and approvals to improve control and avoid duplicate or early payments.

Forecast-to-Fulfill (F2F): Strengthen demand forecasting and align production, inventory, and logistics planning to actual demand.

Cross-functional alignment: Finance, sales, and supply chain must collaborate to avoid working at cross-purposes.

Impact on CCC: Process efficiency reduces friction in all stages of the cycle, accelerating cash inflows and controlling outflows.

5. Monitor KPIs and Trends

DSO (Days Sales Outstanding): Measures speed of customer collections.

DIO (Days Inventory Outstanding): Tracks how efficiently stock is managed.

DPO (Days Payables Outstanding): Shows how long the company takes to pay suppliers.

Cash Conversion Cycle (CCC): The net measure of how effectively operating working capital is being managed.

Best Practice:

Regularly review these KPIs over time and benchmark them against peers and industry standards.

Early shifts in CCC or its components often signal liquidity risks or opportunities before they appear in the P&L.

Go beyond averages: analyze transaction-level data (e.g., invoice-level payment terms, customer payment behavior, supplier invoice patterns).

This provides a true performance view of OWC by uncovering hidden bottlenecks, systemic delays, or exceptions that aggregate KPIs can mask.

Key Lesson

Working capital management is not just a finance exercise – it requires cross-functional coordination.

By combining financial discipline with operational levers such as S&OP, forecasting, and supplier collaboration, companies can reduce the cash locked in operations and turn accounting profits into real, usable cash.

Conclusion

Operating Working Capital and Cashflow are tightly linked. Efficient working capital management frees up cash, reduces reliance on external financing, and supports long-term growth.

Companies that master this balance gain a significant competitive advantage: they are more resilient in downturns, better positioned to invest in opportunities, and less dependent on debt.

In short: profit is important, but cash is survival. Managing working capital effectively ensures both.

Ready to take the next step?

Turn theory into practice and boost your career with accredited training. Become a Certified Operating Working Capital Expert by enrolling in our flagship course: Managing Working Capital.

Working capital is not just a financial metric - it reflects how a business operates. This article explains the key drivers behind inventory, receivables, and payables, and shows how operational

The Cash Conversion Cycle (CCC) is one of the most widely used working capital metrics - but what does it actually measure? This article explains how to calculate the cash

What is a good Cash Conversion Cycle? Most companies treat the Cash Conversion Cycle (CCC) as a race to the bottom - the shorter, the better. But in reality, a